"PEAK OIL TODAY"

The very best weekly analysis and evaluation of the global peak oil situation with additional briefings, charts and videos, added by the curator from accredited professional sources, to enhance the informed investor's knowledge and understanding of its deep complexities and evolving outlooks.

Everyone should "Bookmark ' this very important weekly post to stay abreast of this most critical aspect of global economics and life on this planet.

Peak Oil Review – 7 March 2016

By Tom Whipple

Quote of the Week

About Latin America: “The 70 percent drop in prices is a major shock. Oil was contributing in some countries from 20 to 50 per cent government revenues and 50 to 96 percent of exports. No wonder we are starting to question the financial viability of some countries and some national oil companies.”

Luisa Palacios, head of Latin America at Medley Global Advisors, a risk consultancy

Luisa Palacios, head of Latin America at Medley Global Advisors, a risk consultancy Contents

1. Oil and the Global Economy

2. The Middle East & North Africa

3. China

4. The Briefs

1. Oil and the Global Economy

Oil prices rose for the third consecutive week with New York futures closing at $35.92 a barrel and London at $38.72. Prices in London are now up 3.9 percent for the year. Behind the price rise is a continuing drop in the number of drilling rigs operating in the US and the announcement by several major shale oil producers that they plan to suspend new drilling until prices recover. Exactly where profitability is these days is in dispute with some drillers contending they can make money from shale oil if prices rise into the mid- $40s as compared to $60-70 two years ago. Some of these claims are for the benefit of the banks who have become very wary of the oil industry in recent months. The downside, of course, is that if shale oil producers start increasing production if prices get into the mid-$40s, they could easily drive them back down again with unsaleable production.

Oil’s fundamentals still say that overproduction is alive and well despite small cuts in OPEC and US production in February. The threat of insufficient storage capacity for the excess oil production continues to grow. In the US, the Cushing, Okla. storage facility is now at 90 percent of capacity. In Europe, the large tank farm at Rotterdam has a record number of ships waiting to unload when space for their cargoes becomes available.

Oil’s fundamentals still say that overproduction is alive and well despite small cuts in OPEC and US production in February. The threat of insufficient storage capacity for the excess oil production continues to grow. In the US, the Cushing, Okla. storage facility is now at 90 percent of capacity. In Europe, the large tank farm at Rotterdam has a record number of ships waiting to unload when space for their cargoes becomes available.

The IEA is still saying that supply and demand are unlikely to come back into balance before the end of the year, and even then the world will have 1 billion barrels plus of excess oil in storage that will have to be worked off before significant price increases can occur. Short of export disruptions, most likely to occur somewhere in the Middle East, it may be several years before the markets and the stockpiles come back into balance. On top of this, we have the uncertainties as to where the Chinese economy is going, as bad economic news from Beijing is frequent these days.

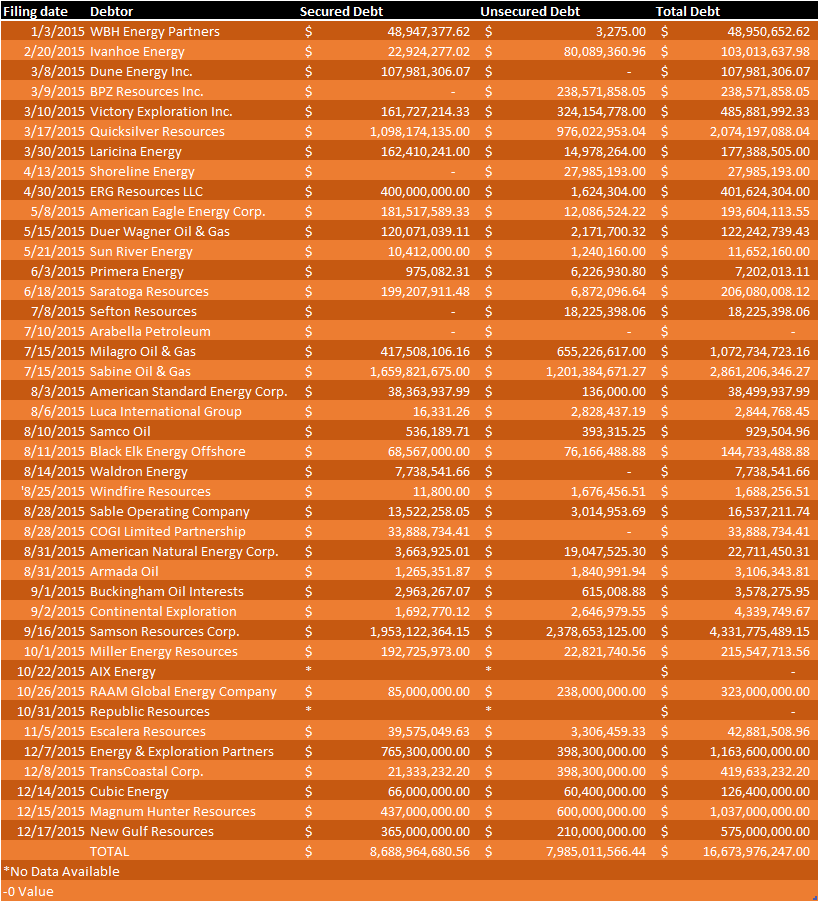

In the meantime, the woes of the global oil and gas industry continue. Some 48 oil and gas producers filed for bankruptcy in North America last year, and more are expected to follow suit in 2016. The newest problem is what happens to the contracts of the “midstream” companies that invested billions in new plants and pipelines to process and deliver crude to refineries. If their oil producers go into bankruptcy, many midstream energy companies will not be far behind as their revenues will dry up. One economist who follows Texas closely notes that the last time oil production was weak there were only about 130,000 people working in the oil industry. This compares to 230,000 workers this January. These numbers imply that we could see another 100,000 Texas oil jobs cut in coming months.

The Wall Street Journal assures us that while the major banks have advanced billions to companies that have or could go into bankruptcy, there is nothing to worry about as the banks are well diversified with much of their oil lending going to the major integrated producers that are likely to pay back their loans. Even in the banks’ worst case scenario under which oil prices fall to $25 a barrel and stay there for 18 months, the banks say they will be all right.

With natural gas futures now priced around $1.79 per million BTUs, a 17-year low, and cash prices in the Marcellus shale now around $1, many producers are clearly losing a lot of money. There is now a record 2.53 trillion cubic feet of natural gas in storage as the winter gas withdrawal season draws to a close and stocks start rebuilding again. If injections into storage caverns this spring and summer are similar to last year, there may not be enough storage space by September. While export demand is growing, it will be several years before this can have a significant impact on the natural gas glut. Unless we have an unusually hot summer, it is likely that many producing wells will have to shut-in during the coming year.

No comments:

Post a Comment